Chapter 8 Value at risk

Value at risk is a measure quantifying risk of investments. It tells what is the maximum potential loss not exceeded with a preset probability (say 5% or 0.1%) over a specified period (such as one day), given normal market conditions.

It is (or used to be) a popular risk measure used by financial institutions.

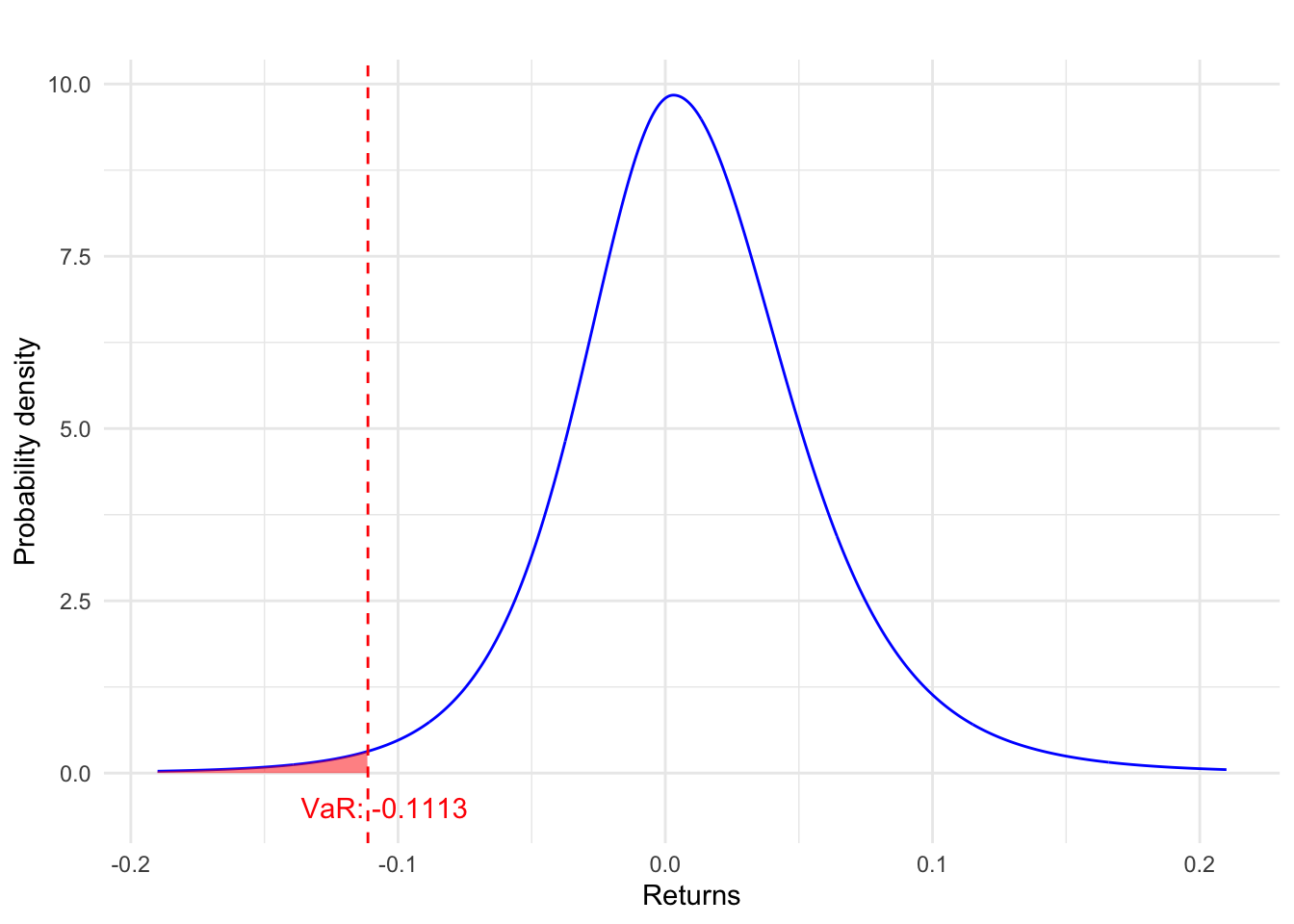

Figure 8.1: Value at Risk (VaR) example